How to Avoid Paying Duty and GST on Imported Gifts

3-minute read

The reference 75 concession allows entry of presents or gifts except tobacco products sent from abroad to a resident in New Zealand:

(i) Not exceeding $110 in total value – Free

(ii) Exceeding $110 in total value, on the excess over $110 – The rates of duty applicable to the goods as set out in Part I of the Tariff. (see examples below)

This concession is intended to cover gifts of a personal nature. A gift is considered to be personal if it:

- is sent to a private person by or on behalf of another private person resident abroad

- is of an unsolicited nature (not ordered or paid for by the addressee)

- is occasional and not part of an ongoing arrangement to avoid the payment of duty and GST

- consists only of goods for personal use by the addressee or his/her family

- the nature and quality of the goods imported are such that the consignment is obviously not of a commercial nature.

Gifts are usually sent from a person overseas rather than a company or business.

However, circumstances may allow the concession to be applied if the goods are sent direct from a business, but can be shown to have been purchased as a gift from the overseas buyer, and shipped directly from the seller on the buyer’s behalf.

Gift parcels (where the contents are intended for more than one person) with a total declared value in excess of $NZ110 may be allowed multiple gift allowances, provided the separate identity of each recipient can be established.

However, the concession may not be combined by multiple persons on one item.

Tobacco products are specifically excluded from the reference 75 concession and full duty and GST is payable on these imports.

Tobacco products are also not covered by the minimum duty collectable exemption.

Alcohol products are not excluded under the terms of the gift concession.

However, because of the high duty rates associated with these goods, Customs must be satisfied as to the unsolicited nature and specific occasion giving rise to the gift and ensure it is not part of an ongoing arrangement to avoid the payment of duty and GST.

The minimum duty collectable exemption does not apply to alcohol products so duty is payable on any excess value of these goods after the concession has been applied.

Application of the gift concession does not reduce the Customs value, or the GST value of the goods, it only reduces the amount of duty and GST that may be payable on the goods after the application of the concession.

Private individuals can approach Customs for assistance in clearing their gifts.

Goods being cleared by brokers or freight forwarders must declare the full value of the goods and then do a manual calculation of the duty and or GST payable on the remaining value after allowing the concession.

Appropriate notes should be entered in the remarks section.

Section 12(4)(e) of the Goods and Services Tax Act 1985 provides an exemption from GST for the goods covered by the reference 75 concession.

This provision allows the portion of the freight and insurance charges relating to the $110.00 value of the goods to be exempt from GST charges.

While the tariff concession applies to the Customs value (on which tariff duty is charged) the GST exemption applies to the GST value* (on which GST is charged) of the same goods, ie, if 20% of the Customs value is covered by the tariff concession, 20% of the GST value of the goods is covered by the GST exemption.

*(GST value is always the total of – Customs value plus duty plus freight and insurance as per section 12(2) of the GST Act).

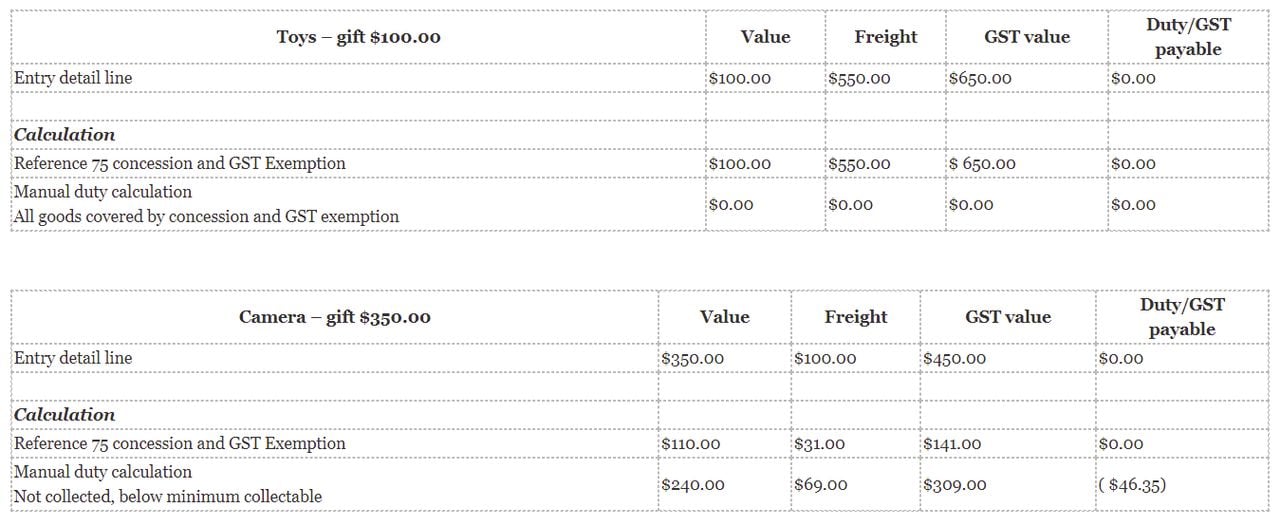

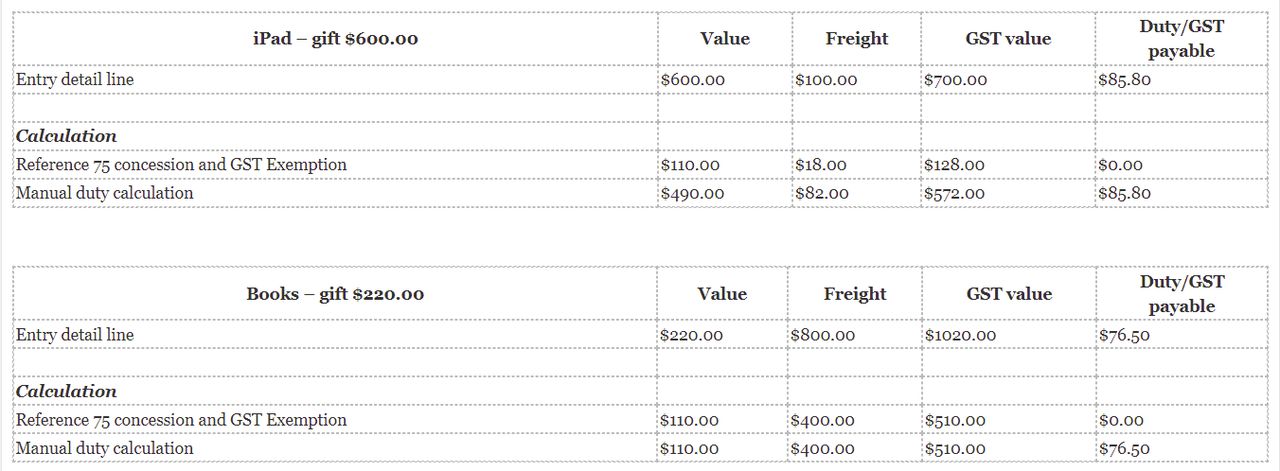

Examples:

Source: NZ Customs

We’d love to answer any of your questions! Contact us now

P.S. Do you know of other people that will find this article useful? Please share it on social media. Thank you!